Scope 1 and Scope 2 Inventory Guidance

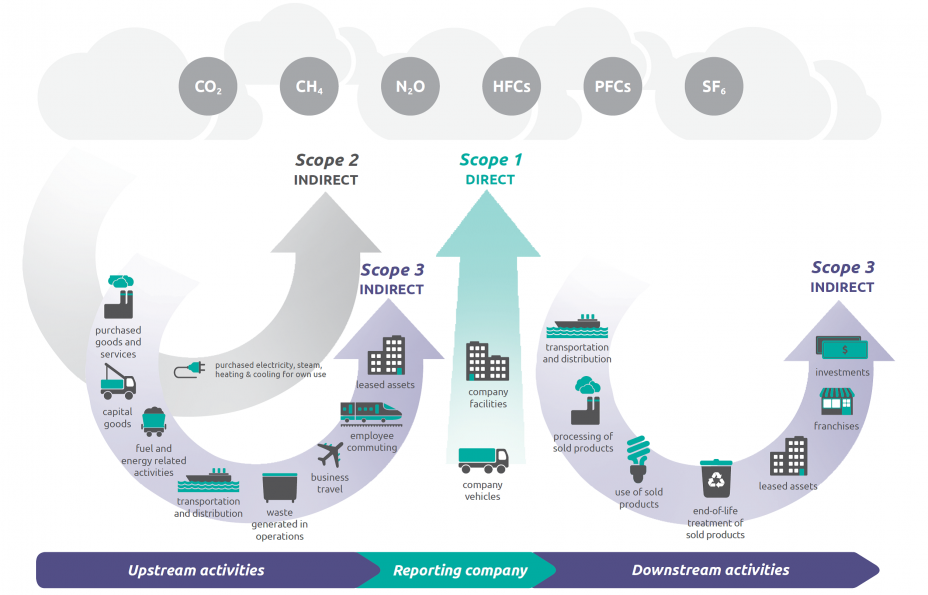

Scope 1 emissions are direct greenhouse (GHG) emissions that occur from sources that are controlled or owned by an organization (e.g., emissions associated with fuel combustion in boilers, furnaces, vehicles). Scope 2 emissions are indirect GHG emissions associated with the purchase of electricity, steam, heat, or cooling. Although scope 2 emissions physically occur at the facility where they are generated, they are accounted for in an organization’s GHG inventory because they are a result of the organization’s energy use.

Overview of GHG Protocol scopes and emissions across the value chain

Source: WRI/WBCSD Corporate Value Chain (Scope 3) Accounting and Reporting Standard (PDF) (152 pp, 5.9MB), page 5.

Source: WRI/WBCSD Corporate Value Chain (Scope 3) Accounting and Reporting Standard (PDF) (152 pp, 5.9MB), page 5.

The following EPA guidance documents describe methods to calculate and report emissions from these sources.

- Direct Emissions From Stationary Combustion

This document is used to identify and estimate direct GHG emissions from stationary (non-transport) combustion of fossil fuels at a facility (e.g., boilers, turbines, process heat). - Direct Emissions From Mobile Combustion Sources

This document is used to identify and estimate direct GHG emissions associated with fuel combustion in owned or operated mobile sources. - Indirect Emissions From Purchased Electricity

This document is used to identify and estimate indirect GHG emissions resulting from the purchase of electricity, steam, heat, or cooling. - Direct Fugitive Emissions from Refrigeration, Air Conditioning, Fire Suppression, and Industrial Gases

This document is used to identify and estimate direct emissions of GHGs from refrigeration and air conditioning systems, fire suppression systems, and the purchase and release of industrial gases.

The GHG Protocol published Scope 2 Guidance Exit that standardizes how corporations measure emissions from purchased or acquired electricity, steam, heat and cooling.

Note: Many industrial sectors also have process-related emissions sources that are specific to their sector. EPA’s Greenhouse Gas Reporting Program provides guidance and tools that can aid in the calculation and reporting of these emissions.