Scope 3 Inventory Guidance

On this page

Description of Scope 3 Emissions

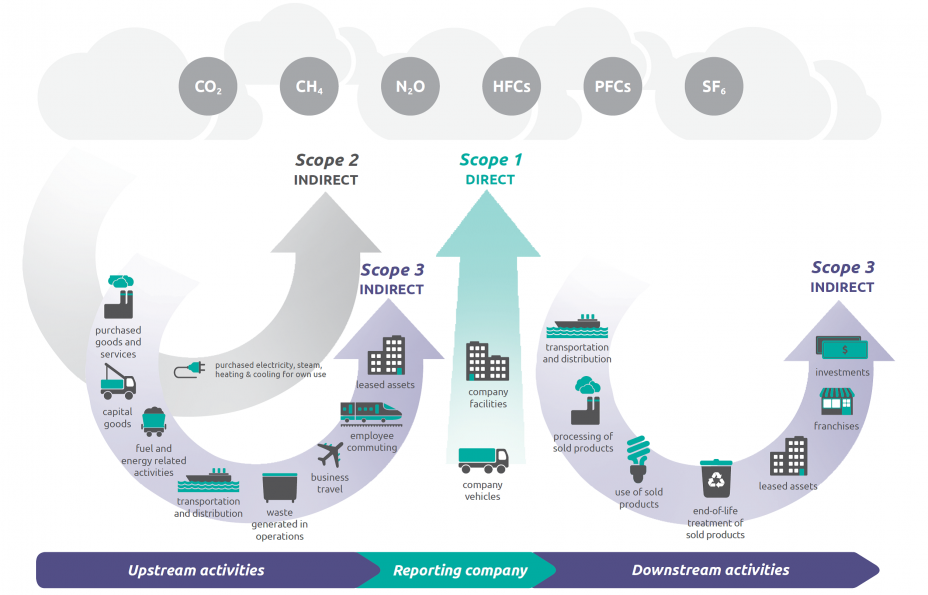

Scope 3 emissions are the result of activities from assets not owned or controlled by the reporting organization, but that the organization indirectly impacts in its value chain. Scope 3 emissions include all sources not within an organization’s scope 1 and 2 boundary. The scope 3 emissions for one organization are the scope 1 and 2 emissions of another organization. Scope 3 emissions, also referred to as value chain emissions, often represent the majority of an organization’s total GHG emissions.

Scope 3 emissions fall within 15 categories, though not every category will be relevant to all organizations. Scope 3 emission sources include emissions both upstream and downstream of the organization’s activities.

According to the GHG Corporate Protocol, all organizations should quantify scope 1 and 2 emissions when reporting and disclosing GHG emissions, while scope 3 emissions quantification is not required. However, more organizations are reaching into their value chain to understand the full GHG impact of their operations. In addition, because scope 3 emission sources may represent the majority of an organization’s GHG emissions, they often offer emissions reduction opportunities. Although these emissions are not under the organization’s control, the organization may be able to impact the activities that result in the emissions. The organization may also be able to influence its suppliers or choose which vendors to contract with based on their practices.

For a complete description of all scope 3 categories and quantification methods, see the GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard Exit.

Overview of GHG Protocol scopes and emissions across the value chain

Source: WRI/WBCSD Corporate Value Chain (Scope 3) Accounting and Reporting Standard (PDF) (152 pp, 5.9MB), page 5.

Source: WRI/WBCSD Corporate Value Chain (Scope 3) Accounting and Reporting Standard (PDF) (152 pp, 5.9MB), page 5.

Scope 3 Resources

The GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard Exit presents details on all scope 3 categories and requirements and guidance on reporting scope 3 emissions.

The GHG Protocol also provides the following additional scope 3 resources:

- Guidance for Calculating Scope 3 Emissions Exit for each category, including guidance on required data, data collection methods, and quantification methods

- The Scope 3 Evaluator tool Exit to help organizations screen scope 3 emissions categories to identifying focus areas

- Guidance for calculating scope 3 emissions resulting from events (e.g., sporting events, concerts) and conferences (e.g., business meetings, exhibits, conventions). The emissions sources covered include: travel to and from an event, emissions from hotel stays by attendees, and emissions from the event or conference venue.

Depending on the source, scope 3 emissions can be quantified using either primary data specific to the activity within a company’s value chain, or by using secondary data such as industry averages, proxy data, or other generic data. Primary data must often be collected directly from suppliers through a questionnaire or similar format.

Scope 3 Emission Factors

EPA currently provides certain scope 3 emission factors. The sections below discuss the currently available emission factors and how to apply scope 1 and 2 factors to calculate scope 3 emissions for certain categories. The categories listed are those defined in the GHG Protocol Scope 3 Standard Exit.

Emission Factors Currently Available

The GHG Emission Factors Hub currently contains factors applicable to five scope 3 categories. Below is a list of emission sources and the location of the factors in the GHG Emission Factors Hub.

- Upstream Transportation and Distribution (Category 4): Table 8

- Downstream Transportation and Distribution (Category 9): Table 8 1

- Waste Generated in Operations (Category 5): Table 9

- End-of-life treatment of sold products (Category 12): Table 9

- Business Travel (Category 6): Table 10

- Employee Commuting (Category 7): Table 10 2

Emission Source Categories Using Scope 1 and 2 Emission Factors

Some scope 3 categories do not require specific emission factors, because the emissions-generating activities have associated scope 1 and scope 2 factors already available in the GHG Emission Factors Hub. These sources include:

- Upstream leased assets (Category 8)

- Processing of sold products (Category 10)

- Use of sold products (Category 11)

- Downstream leased assets (Category 13)

- Franchises (Category 14)

- Investments (Category 15)

An organization may first define the GHG generating activity for each relevant source category, and then apply the appropriate factors for stationary combustion, mobile combustion, fugitive emissions, electricity, heat or steam from the GHG Emission Factors Hub.

For example, assume your organization produces electronic equipment. The downstream use of sold products (Category 11) may likely be a large source of emissions. In order to calculate emissions, estimate the lifetime electricity consumption (kWh) for all products sold in the reporting year. Then calculate emissions the same as for scope 2 electricity, using eGRID emission factors. Depending on the data available for the location of product use, eGRID subregion or U.S. national average factors would be applied.

1 These factors are applicable to all transportation; upstream or downstream, product-related or not.

2 These factors are applicable to employee commuting as well as business travel.